EDF's woes are a bigger long term problem for EU energy than the war in Ukraine

France is looking at many dark years

The war in Ukraine is undoubtedly causing an energy crisis. It will have a potentially severe impact on the heating sector (muted for now as we are in the warm season) and has an immediate one on industry (via price increases for gas and talk of curtailment), but it is actually not the main driver of what’s happening in the electricity sector in Europe. All the criticism one can hear about Germany’s decision to close down its nuclear plants misses the fact that gas availability is not the problem for the power sector: the real problem is the unavailability of French nuclear.

If you look at Germany’s power production (here, presented as a percentage of total electricity production), you see that the share of gas (around 15%) and coal (around 28%) have barely budged between 2021 and 2022, while nuclear was cut in half (from 11% to 6%), and the difference was taken by increasing renewables penetration. In other words, the gas price increases should have caused power price increases only at peak times, and not across the board.

Source: Axios, Europe's surging electricity prices are shattering records

Source: NGI, European Supply Tightness Boosts Gas Prices

And yet prices for electricity have gone up massively and for much longer periods than one would expect from a mere disruption to gas availability.

The absolute levels reached for power prices are definitely linked to the much higher gas prices (a normal consequence of power prices being linked to the marginal cost producer, which is usually gas), but the breadth of the increase has other causes.

Indeed, looking around Europe, one can see that the price disruption is not uniform, and not what one could expect:

Source: RTE market data

Spain has relatively low prices. Some of that is linked to the price caps put in place, but it’s an isolated market that relies significantly on gas prices and is heavily exposed to international LNG prices given its strong regasification capabilities - so one could argue that this is what the consequences of higher gas prices should look like, overall, in a ‘normal’ market (after discounting for the price cap effect, which does not modify the underlying spot price).

Conversely, France now consistently has the highest power prices in Europe, despite in principle having the least fossil-fuel dependent generation fleet. That comes from no longer having enough generation capacity available.

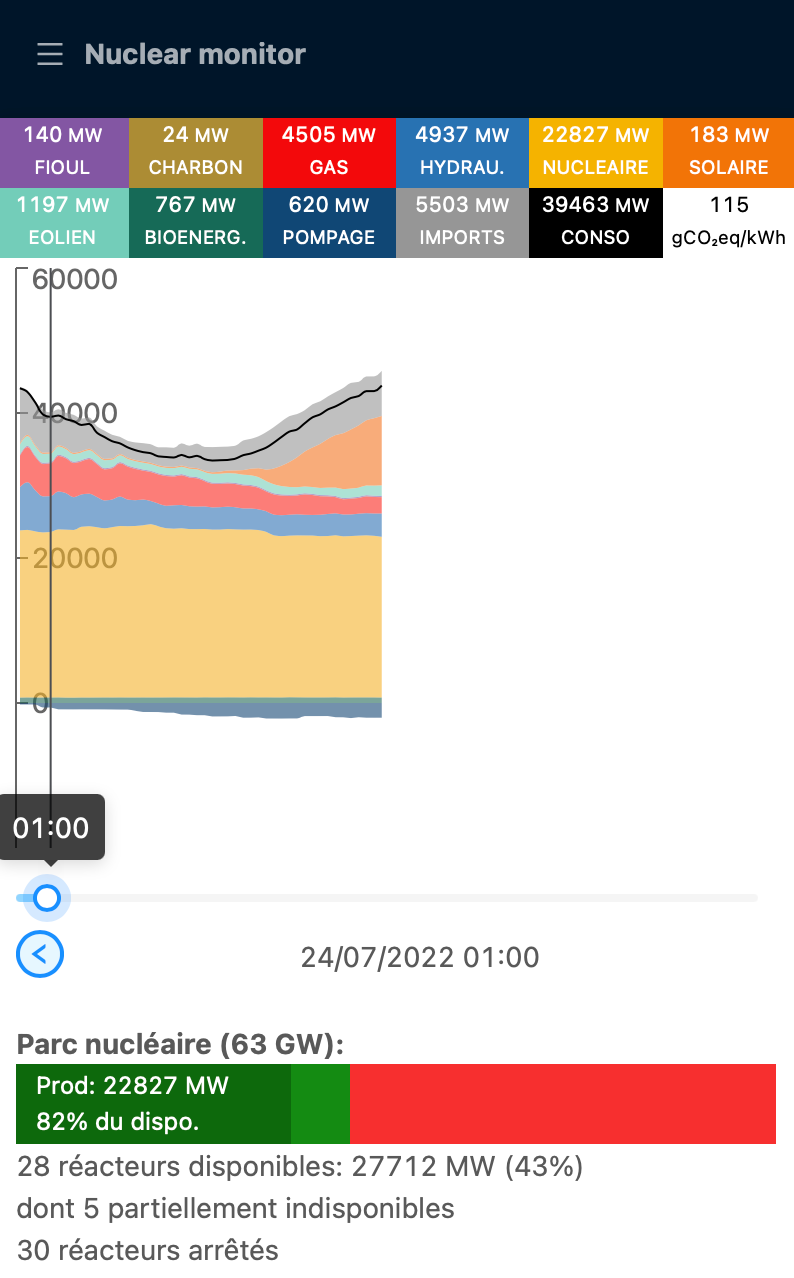

As the right-hand side numbers above show, even in the middle of a summer week-end (this Sunday 24 July at 1am), when demand is supposed to be near its lowest, and should be fully covered by ultra-cheap baseload such a nuclear, prices remain incredibly high in France, and “pollute” nearby areas, as France needs to import power even at that point in time - and throughout the day:

Source: Nuclear monitor

In fact, France’s nuclear fleet, with a theoretical total capacity of 63 GW, has not been cranking out more than 25 GW in recent times. Summer is a traditionally lower demand period in France, so a lot of maintenance is done at that time, and you would not expect the full capacity to be available, but you’d definitely expect enough to deal with domestic demand and some exports - but no, even at the time of peak prices in the middle of last week, production was still constrained:

Source: Nuclear monitor

Some specific, temporary, factors have played a role (like restrictions on water use during the recent heat wave), but overall, the French nuclear capacity is increasingly constrained and unable to provide for French demand. As a result, France is becoming an importer of power - a lot of the time, and increasingly, on a net basis (after years of being the largest exporter in Europe), pulling in supply from neighboring countries that used to rely on French surpluses and increasing the tensions there at a time when these countries are themselves under specific stress due to the higher gas prices:

Source: FT, EDF’s problems pile up as full nationalisation looms, 17 July 2022

As noted, summer is the traditional maintenance period for EDF, but 12 reactors (out of 58) are currently offline due to corrosion issues, and it’s not clear when these will be sorted out, as some seem to be structural are may require complex re-design (I expect discuss this in a separate post soon). The result is a material decline in overall generation, amplifying a trend that started a few years ago, with production set to reach about only half of the nuclear fleet’s theoretical maximum production capacity (63 GW at 100% capacity would generate 550 TWh in a year; the highest ever in practice was 450 TWh in 2005, a capacity factor of 82%)

Source: FT, Power plant shutdowns hinder France’s ‘nuclear adventure’ (17 May 2022)

That’s close to 100 TWh per year missing from the market, equivalent to the sum of what Germany produces from its nuclear and gas-fired power plants!

Thus the high prices in France, needed to draw power from markets that would otherwise not naturally export in such volumes (indeed, they would usually import cheap French nuclear power), and see their own market balance strained. France having become a net importer, with the highest price most of the time, shows conclusively that it is the lack of generation capacity in France that drive higher power prices in all neighboring countries.

The question then becomes: is this a temporary situation, or something more permanent?

Some of the answer is linked to the resolution of the corrosion issues in some of the French plants. That may end up becoming a political decision, to let these plants start production again, even if the issue is not fully solved, by accepting a higher level of risk on these plants, in order to bring back some much needed generation capacity and reduce the pressure on power prices.

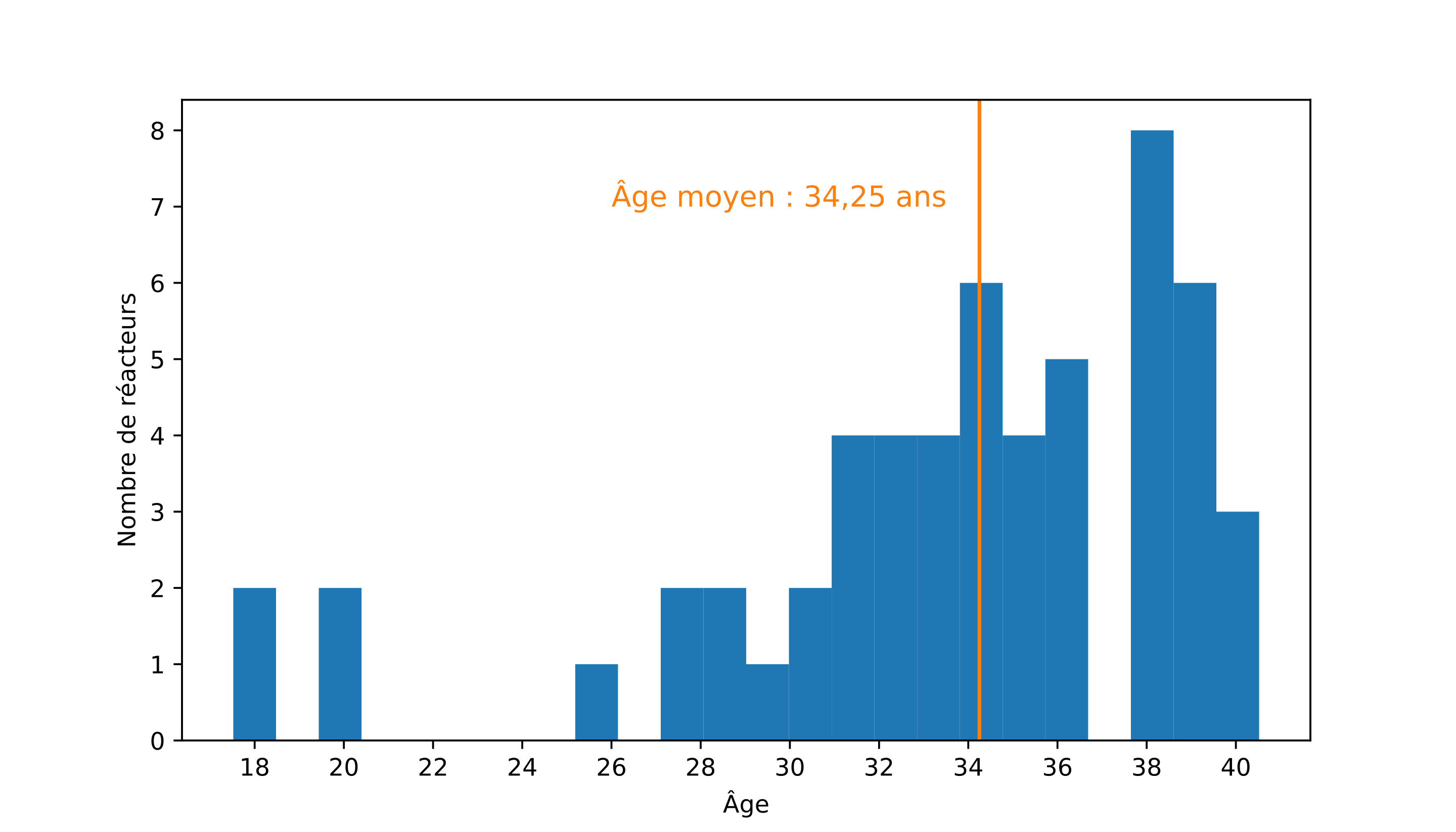

But even if this problem is solved, or pushed under the carpet, and this leads to a reprieve on short term power prices, the long term issues of having an increasing old nuclear fleet are getting worse each year. With an average age now above 35 years, French nuclear plants are becoming increasingly costly to operate.

Source: Wikipedia, Age of French nuclear plants (in 2020)

{kind=link}

That means potentially increasing outages as production-stopping incidents increase (although it should be noted that ironically, the corrosion issues have affected the youngest plants) and generally lower fleet availability as large scale maintenance needs to be performed, such as the grand carénage heavy maintenance/upgrade required to extend the operating life of each plant.

And the problem is that nothing is getting built to replace these plants. The next generation EPRs were supposed to take over, but the first one in Flamanville is now over 10 years late (without a firm date yet to be put in service, and a quadrupling at least of its construction costs), and its cousins in Finland, the UK and China have all suffered from serious problems and delays, meaning that the large scale construction of new plants (even assuming that all technical problems with the early EPRs get sorted out) has also been correspondingly delayed, with an accompanying loss of skills as people have left the industry, and high uncertainty as to future costs.

Renewables have not been built on as large scale as would have been possible in France, given the argument (reasonable, for a long time) that France already had cheap and decarbonated power generation. New projects continue to be plagued by local hostility - which has become, if anything, stronger than before even as renewables projects became more competitive. Some new solar and onshore wind capacity continues to get built each year, despite the hostility, but nowhere near the volumes that would be needed. Tenders for offshore wind, in particular for floating capacity, are being programmed, but the volumes are nowhere near sufficient to replace a meaningful part of the nuclear capacity, and timing is still highly uncertain - the first generation of offshore wind projects, tendered in 2011 and 2012, are only being built now, with 10 years of delays due to legal action by opponents. Rules have been streamlined, but the new processes are still untested.

So we could be facing a period of 10-20 years when France becomes structurally unable to produce its own electricity in full, and has to rely on imports from neighboring countries, reversing the pattern of the past 30 years and straining the whole European power markets.

The recent decision by the French government to nationalise EDF is an implicit acknowledgment that this is becoming an existential crisis for the company and the country. The war in Ukraine is masking to some extent how deep the problem is (by hiding it behind an equally intense, but likely less long, crisis), but this is likely to become a core part of Macron’s to-do list throughout his second 5-year term, and it will definitely trigger an ugly debate in France, given how unprepared the political class is for this energy transition.

And given how large the hole caused by France’s vanishing nuclear fleet is, all of Europe will be drawn into that crisis.

Update, 4 August 2022: See my follow up post:

This is the best piece I’ve read, by far, on the issue. Excellent!

Brilliant article! Apart from the generation side, what is rarely discussed is lowering demand altogether, because the greenest form of energy is the one that isn't used. Energy efficiency and grid improvements can make up to some degree for lost generation. Not only to connect demand centres with large generators within a country, but also to create better interconnectors between countries where renewable power from one country can be used in an other. This would lower renewable energy curtailment and allow for more flexible demand response. Thank you Jérôme à Paris, you have one more subscriber.